It has been a curious coincidence that the extraordinary Damien Hirst sale took place just before global finances collapsed. It might have happened on a different planet. Yet it has been possible, now both dustbowls have settled momentarily, to weigh up the connectivity of each circus round.

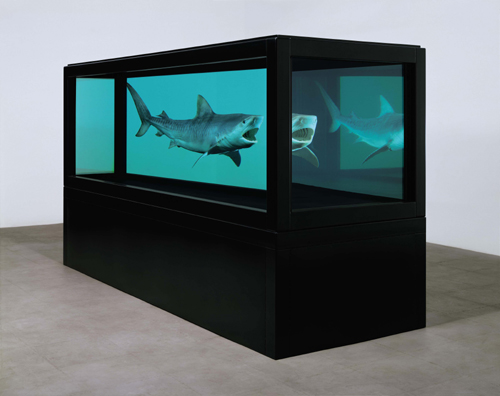

The key pundits have been hunched around the screen of the soaring prices for the Damien Hirst works raised at the two Sotheby's sales in London on Monday 15th September and the following day. That Monday was also, ironically, the day when the New York brokers Lehman Brothers were forced to opt for bankruptcy. What both events had in common was the activity of hedging, said to have precipitated the New York market collapse. Hirst's prices were openly supported by a purchasing operation mounted by his dealers. Although Hirst had declared that the sales were a means by which he could effectively break away from his dealers, in actual fact the White Cube gallery bought some £7 million of art works, going way over the estimates. As well as being the underbidder for 'The Kingdom' - the tiger shark sunk in a steel tank, eventually sold at £9.6 million - White Cube were identified as underbidders on some £20 million of art works overall. Gagosian, Hirst's New York dealer, was the underbidder for the calf in a golden case, sold at £10.3 million. Of course these dealers, including Haunch of Venison gallery owner Harry Blain, were arguably serving their own lists of clients desperate to acquire a work by Damien Hirst. But the clear evidence was of a sophisticated support operation in full swing, also maintaining the value of collectors' bought stock. There was nothing accidental, which cannot be said of Wall Street's own downward cascading.

In 1982, a searching appraisal of the development of the historical art market was published in London by one Joseph Alsop, a well-connected sage on the London and New York art historical circuit and deliverer of an earlier Andrew Mellon Lecture in Fine Arts in 1978. The work was entitled 'The Rare Art Traditions'1 subtitled 'The History of Art Collecting and its Linked Phenomena Wherever These Have Appeared.' What was interesting about this work was the way in which Alsop analysed what he called, 'The integrated behavioural systems created as the by-product of art'. He found that these activities could be broken down into the following main categories: art collecting, art history, art market, art museums, art faking, revaluation, antiques and the phenomenon of 'super prices'. Collectors, he found, established all their own 'categories', to be subject to a controlling role. Alsop also traced the activity of such masters as Titian and Bellini, for example, in 'painting for stock', an activity pursued by artists as early as the 16th century. Of course, Alsop was writing at the point where the 'museum age', so-called, was at its climax, and museum directors themselves held sway in the field of not only establishing value, provenance, and controlled acquisition through the sale rooms. He quoted the case here of de Kooning, and the earlier 'anti-art' role developed by such as the Dadaists and Marcel Duchamp. But what Alsop could not predict accurately was the extent to which artists might eventually (qua Damien Hirst) bypass the dealers completely, or render them into a supplicant 'support', 'hedge fund' acquisition or underbidding role within the saleroom. This has now happened, and the big question for the art market is, 'Where next?' One result may be that while key works spiral onwards and upwards in price (based upon the law of supply and demand, coupled with clear 'branding' of the artists' products), the secondary, sub-prime works may equally surely spiral downwards in value.

It may have been noted that there has been no discussion introduced here yet about the actual intrinsic quality of the Hirst works. The renowned art critic Bob Hughes has weighed in here. In a recent film for UK Channel 4 television, 'The Mona Lisa Curse',2 he very eruditely canvassed a broad constituency of New York dealers/curators from the 1990s, arguing that, 'Art was the biggest unregulated market in the world apart from drugs.' 'Modern art' he said 'is dottily expensive to buy not because it's so good but because investors believe it will yield quick profits.' As Hughes says, it is the museums that are priced out of the market. This recognises even though at an earlier stage in the establishing and recognition of the value of an artist and his/her work, the museum curatorial judgment may have been crucial. Hughes also casts doubt on the concept of the inviolability of art prices. On the issue of 'faking' commented on by Alsop, it can be separately added here that the celebrated contemporary graffiti artist Banksy has this month claimed that there are a flood of fakes of his work now in circulation. No surprise.

The price of a work is now part of its function but the museums have been inevitably increasingly squeezed out of the market. The Director of the Metropolitan Museum, New York, Phillippe de Montebello, told Hughes that in a Wall Street parallel on the 'moment in history', for the moment, the Met was out of the market. The great period of museums was over. The touring of the 'Mona Lisa' from the Louvre to New York from 1962 marked this geological shift forever in the art and museum world.

This is the true significance of the recent Sotheby's sales of Hirst's work. A moment of comparable significance to that has now occurred, with long lasting, deeply rooted effects. Joseph Alsop did not actually directly forecast this sea change, but it has direct reference bearing upon his earlier analysis of 'The Rare Art Traditions.'

Michael Spens

References

1. Alsop, J. The Rare Art Traditions. London: Thames & Hudson Ltd, 1982

2. Broadcast as 'The Mona Lisa Curse'. Channel 4, 21 September 2008.

Click on the pictures below to enlarge

Copyright © 1893–2026 Studio International Foundation.

The title Studio International is the property of the Studio International Foundation and, together with the content, are bound by copyright. All rights reserved.

-300.jpg) Painting Now: Five Contemporary Artists

Painting Now: Five Contemporary Artists Art Under Attack: Histories of British Iconoclasm

Art Under Attack: Histories of British Iconoclasm George Gittoes

George Gittoes Rodin

Rodin In the Kingdom of the Gods and Goddesses

In the Kingdom of the Gods and Goddesses